Navigating Your Finances: Budgeting Basics for Beginners

Take a look at how you can start easily start a budget that isn’t overwhelming or complicated.

2/12/20244 min read

Welcome back, and say hello to the wonderful (or not-so-wonderful) world of budgeting. Whether you're just starting out on a financial journey or looking to brush up on your money management skills, understanding the basics of budgeting is the #1 most essential step. This can feel daunting after a quick Google search, but let’s break it down together.

What is Budgeting?

At its core, budgeting is simply a way to track your income and expenses to make sure that you’re living within your means and using your funds efficiently. There are a million different ways to budget, and they can get royally complex. But we’re just going to think of it as a roadmap for your finances, helping you prioritize your spending, set financial goals, and ultimately, make better decisions with your money.

Know Your Numbers

We talked about this in the last post: Top Tips for the Average Person to Save Money and Avoid Impulse Spending. I said it then, and I’ll say it again; prepare to get your feelings hurt. The first step in creating a budget is to look at your current financial situation with a magnifying glass. Gather up your bank statements, pay stubs, credit card bills, and any other relevant financial documents to get a clear picture of your income and expenses.

Start by listing out all of your sources of income, whether it's your salary, freelance gigs, or side hustle earnings. Don’t leave anything out! Next, jot down all of your monthly expenses, from rent and utilities to groceries and entertainment. Be sure to include both fixed expenses (those that stay the same each month) and variable expenses (those that fluctuate).

Once you have a clear picture of your income and expenses, it's time to do some math. Subtract your total expenses from your total income to determine whether you're operating at a surplus or a deficit. Don’t panic if you’re spending more than you’re earning - I guarantee most people were when they first started budgeting. I’ve budgeted for several years and still end up with months where I spend more than I bring in. If this is you, we’ll tackle that in the next section.

Where Do You Want to Go?

Now that you have a good idea of where your finances currently stand, it's time to think about what goals you have and what you want to accomplish. Do you want to save for a big vacation or a downpayment for a home, pay off debt, or build an emergency fund? If you have multiple goals, list them out by highest priority. Then, once you accomplish the first, you can seamlessly start on the next.

Whatever your goals may be, it's important to make them specific, measurable, achievable, relevant, and time-bound – aka SMART goals. For example, instead of saying "I want to save money," say "I want to save $1,000 for a summer vacation by December 31st." I've used blanket statements before and they never work, mainly because there's no accountability by a time-bound or measurable goal.

Make It Work for You

Bring your goal list, and it's time to crunch some numbers. The first and most important fund bucket goes towards your essential expenses – things like housing, food, transportation, utilities, and debt payment minimums. These minimums are necessary payments, so we're including these here, even though they don't count as a basic living necessity!

Most gurus and experts would advise that your next bucket go towards your goals, and the last bucket go towards your wants. I disagree. Why? Because in my experience, setting your interests and wants aside can very easily derail your progress and result in overspending. For those who have tried dieting or losing weight previously, this works the same way as heavily restricting the foods you enjoy. What ends up happening? You snap and eat three days' worth of snacks in one night. It's the same with spending. So, the next bucket is allocated for the things that you enjoy, but within reason. Don't go crazy and set aside $1,000 for massages and pedicures and then only have $100 remaining for your goals. Try and create a healthy balance.

The remaining income should be set aside for your goals: debt repayment, emergency savings, vacations, or whatever you have written down in the #1 spot.

Stay on Course

Dude, you did it. You've created your first budget and it wasn't even that hard! Unfortunately, the work doesn't stop here, though. For your budget to be effective, you'll need to keep track of your spending and adjust your budget as needed. I typically check in on how my budget is shaping out two or three times a month. Frequently enough to know where I am and to stay in line, but not obsessively. Just keep in mind that budgets can be fluid and don't need to be 100% fixed. It's okay to go back and make adjustments if you have extra money coming in or if your paycheck will be a little short, unseen expenses come up, whatever it may be. These budget strategies are meant to work for you, not against you.

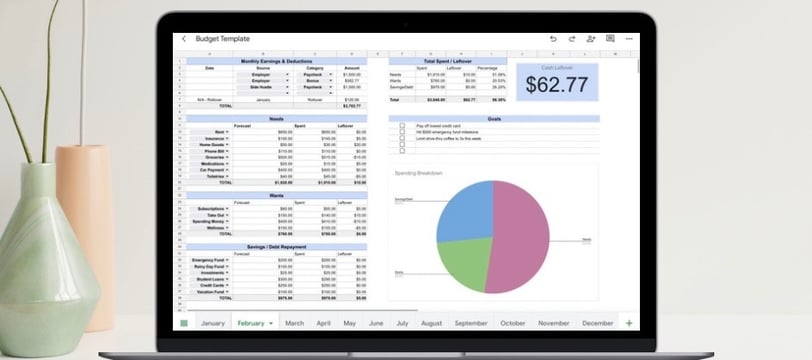

To help stay on course, consider using a budgeting app or spreadsheet to track your expenses in real time. I have a version of the budget spreadsheet that I created and use regularly available for purchase in the store linked here. It’s adjustable and able to be personalized for your individual situation, and helps give you a big picture of where your money goes by breaking it down and calculating it into a chart to be more easily consumed. Regardless of what you use, some form of tracking tool is a necessity to identify any areas where you may be overspending. Remember, budgeting is a dynamic process!

You Deserve It!

Finally, don't forget to celebrate your progress along the way. Celebrating small milestones will keep you motivated to keep your progress going! Some milestones can be hitting your first $500 or $1,000 in a savings fund, paying off a credit card, or simply making your first month without overspending. It's most fun when you determine how you'll celebrate ahead of time so that you have something to look forward to. Example: go out to dinner at your favorite restaurant, make a social media post, call your mom. Doesn't matter what it is, as long as it doesn't derail your progress and it excites you.

In closing, there you have it – the basics of budgeting. That wasn’t so hard, right? Maybe it was, but I believe in you. Remember, Rome wasn't built in a day, and neither is financial security (even though I wish every day that I woke up wealthy). Keep on keeping on!